Dear Friends,

Good afternoon. Venky here from Agribusiness Matters. Welcome to the Sunday digest edition, where I reflect and ruminate over the previous week’s newsletter.

“It was the best of times,

it was the worst of times,

it was the age of wisdom,

it was the age of foolishness,

it was the epoch of belief,

it was the epoch of incredulity,

it was the season of Light,

it was the season of Darkness,

it was the spring of hope,

it was the winter of despair,”

There was a point in my early adulthood days when I felt compelled to start almost every other long form essay with these memorable starting lines from Charles Dickens’ famous novel, A Tale of Two Cities.

Thankfully, as I grew older, I realised that you can’t stretch further beyond a point to draw lessons from a tear-jerker that talked about the miserable lives of those who lived in London and Paris in the early days of the French Revolution.

Even though it seemed tempting to commit glib thievery and steal the original title of the novel to narrate the tale of Agtech revolution happening in the Indian cities of Bangalore and Hyderabad, the former blazing with its youthful exuberance of being the Agtech Startup Hub, while the latter takes measured steps, being the mature adult donning the mantle of the Agribusiness Hub and the Seed Capital of India, I tossed away this thought to the dustbin with no mood to narrate a tale full of sound and fury with reductive proportions.

But here is the thing.

No matter how hard I try to avoid dickensian references, I can’t shake off the feeling that the Agtech India story today so far sounds more or less like those opening lines.

We seem to be living through an age of extremes.

At one end, the amendment of APMC is celebrated by Agtech lobbies, vying for centralisation of the “state subject” of agriculture and economists as a watershed “1991 moment” in Indian Agriculture (that is, assuming you discount the voices of environmentalists like Ashish Kothari who wonder if “1991 moment” should be celebrated in the first place)

And at the other end, the amendment is condemned by political scientists and farmer welfare interest group leaders who wonder how can free markets function in agriculture when it has failed to be efficient in the case of US/EU, especially when the structural barriers for farmers to access the market remains high.

Net net, it becomes a chicken-egg question.

Do you open up the markets with the hope that the infrastructure that the government has budgeted for post-harvest storage (Rs one lakh crore for building agriculture infrastructure to Rs 500 crore for beekeeping and another Rs 500 crore for tomatoes, onions, potatoes, and other fruits and vegetables and so on) is fully developed alongside private player investments and FPOs for the key stakeholders to come together and make economic sense at scale?

Or do you make the infant industry argument and demand for state intervention until the necessary infrastructure gets built to create a level-playing field between farmers and the aggregators?

Depending on which argument you find yourself nodding your head vigorously for, you could very well get sucked in narrating the tale of two competing visions for the future of agriculture.

If you carefully look beyond your biases and really observe what's happening on the ground, two visions about the future of agriculture have been quietly playing out, competing with each other.

Vision #1: Small land holding farmers don't matter in the long run, as their farms will be eventually consolidated by the market economics of digital agribusiness.

Vision #2: Small land holding farmers matter in the long run, as it is morally important to protect agriculturists and their fragile cultural ecosystem from digital agribusiness.

I say quietly because this has been more often implicit than explicit, especially, in the case of Vision #1. Although, there have been few instances when this has been made explicit by economists.

Although many agritech professionals I know have invested in Vision#1 and have been more or less vocal about picking their sides, being an independent agritech consultant, I have the freedom to work towards both vision #1 and vision #2.

Similarly, closer home, if you look beyond your biases and really observe what's happening on the ground, two visions about the future of agri input commerce have been playing out, competing with each other.

Vision #1: Traditional Agri-Input Retailers don't matter in the long run, as they never had the right skin in the game in the first place, often colluding with agri-input manufacturers at the expense of farmers.

Vision #2: Traditional Agri-Input Retailers matter in the long run, as it is impossible to serve farmers in a vacuum and ignore the complex web of relations they are enmeshed in.

Those who've read my blogs regularly know my bias towards vision #2, although off late, I've begun to recalibrate my vision, given the growing prominence of Farmers Business Network (FBN) as a poster boy embodying Vision #1.

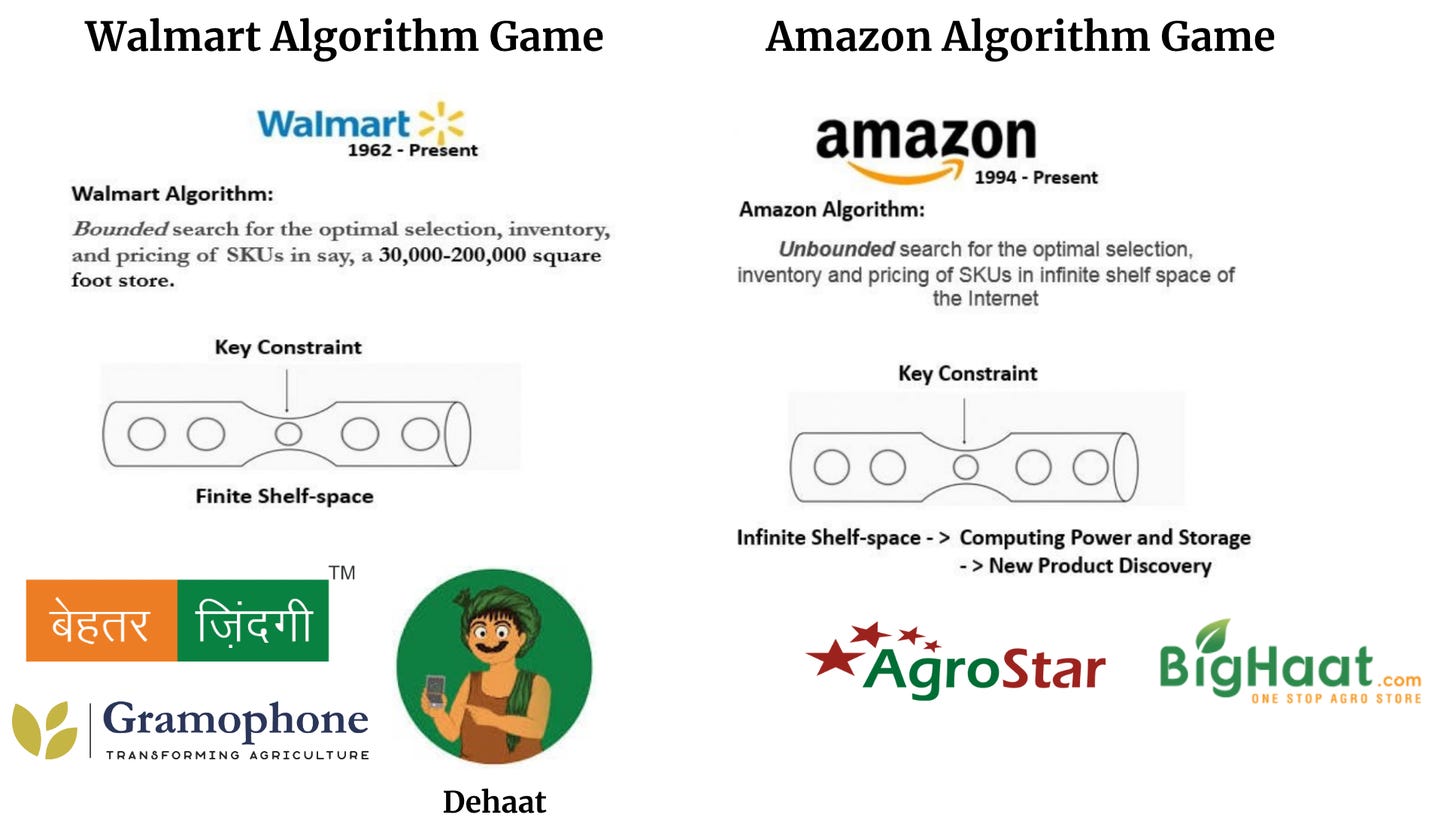

Last week, I wrote about two algorithm games that are playing out in the emerging world of agri-input retailing.

Here is a quick visual summary of the algorithm games and the agtech startups that are betting on them.

Although I had made a bold argument in that article stating that only the Walmart Algorithm Game will be profitable in the long run, taking into account the unit economics involved in serving individual farmers, I am beginning to wonder if my argument could be turned upon its head, given the recent amendment of APMC.

After all, if the farmer gets access for his commodity to different markets, then he will purchase also from different markets, without depending upon his local pesticide shop. Would this alter the unit economics of serving farmers at mandal and village level? How would this vary the credit flows?

We will have to wait and watch.

Nevertheless, when I connect the dots between the two visions of agri-input commerce and the two algorithms that seem predominant in retailing, very interesting insights starts to emerge.

Those who are aspiring towards vision#1 in the future of agri-input commerce seem more inclined to integrate backwards and disrupt the purpose of agri-input manufacturers in agribusiness, while those aspiring towards vision#2 seems more inclined to integrate forward so that they could offer credit to retailers and farmers in that particular order of priority.

That’s all for today!

Do share this newsletter if you found it valuable.

Do you find yourself strongly disagreeing with my perspectives? Join the conversation below in comments.