Thus spake sufi saint Hazrat Zaheen Taj in one of my favourite poems:

“Pani-Pani rat'te rat'te pyaasa hi mar jaaye!”

Chanting 'water', 'water' endlessly, one dies of thirst

We have been talking about the idea of buying directly from farmers for a very long time, while buying from traders, wholesalers, MNCs and everyone else. Are we now finally entering the phase where this possibility is lot more closer to probability and, ergo, reality?

If you want to bring smallholding farmers closer to consumers thereby ensuring that farmers have great livelihoods to grow great food for consumers, what would be your strategic focus - Value Chain, Technology or Branding? Of course, there is no one right answer. The question is - How do they all add up?

Few weeks ago, along with ABM Members Vishalakshi, Reshmi and Akshay (chiming in to explore quick-commerce collaborations), I organized “State of Direct-to-Farmer Trade Commerce” ABM Townhall with three founders working on bringing farmers closer to consumers from three different vantage points - value chain, branding and technology.

Nitin Puri, Founder Kisaansay (Branding)

Ruchit Garg, Founder, Harvesting Foundation (Technology)

Rahul Prakash, Founder and CEO AmalFarm (Value-Chain)

KisaanSay and Amalfarm have been building the place-of-origin promise marketplaces in collaboration with thriving farmer producer organisations in the country. Harvesting Foundation has been building HFN Mandi to help large number of farmers brand, market & sell their crops and also focusing on agri-input supply chains, building Kisaan Saarthis (Farmer aggregators) across their farmer networks.

What are the challenges in sourcing from farmer enterprises? Can we build truly farmer-owned brands that can reach global markets? Why does Amalfarm focus on GI-tagged products? Do farmers get better margins in place-of-origin products? How do we strengthen the ecosystem to make "One District One Product" initiative a success?

Nitin Puri, in a chat, once told me that "We're building Amul 2.0 at KisaanSay, and Dr. Kurien & the Amul model are our inspiration". What is Amul 2.0 model? In what ways does Amul 2.0 diverge and converge from Amul Model?

A lot of promise is riding over Indian Farmer Producer Organisations (FPO) at the moment. How do we manifest this promise? What is required to make FPO promise deliver better livelihood options for farmers?

After sufficiently exploring each these questions with this wonderful panel, I discovered few fascinating insights that made me ponder deeply about the problem at hand and the solutions we are attempting to bridge this vast chasm between the rural farmer and urban consumer.

“We somehow divide ourselves into two worlds. One is the typical NGO development sector way of working. And the other extreme is the way market forces work and large corporations work. And because we divided ourselves into two different zones or partitions, we've never been able to cross-fertilize the kind of ideas, thoughts, people, system, processes into one concrete holistic model” - Nitin Puri

We have food security. We don’t have nutritional security. How do we solve for nutritional security at scale?

Does buying directly from farmers mean anything to the average consumer who values price, taste, convenience over anything else? Or is there an emerging segment of consumers who are equally tired of false promises of “organic” and large multinational brands offering certified, regulated food with pesticide residues and are eager to figure out alternatives to provide healthy, trustable food to their families?

When you are want to bring technology to solve problems at farmer village level, the problem statement is this - How to make farmers co-operate without having to form real cooperatives?

When you are focusing on bridging farmers with consumers, figuring out the model to sell one metric ton is the holy grail to build strong farmgate ecosystems.

Grading needs to be done at farmgate, especially to ascertain the conversion ratio for primitive rice varieties.

Logistics is a real pain point - How do we solve for delivery when farmer lives in regions where no courier services are ready to pick up? How do we reach to the 80% of the 19000 pin codes in the country?

When you want to solve for direct-from-farmer “branding” with the existing value chain infrastructure available in the country, building a supply chain with the trifecta of transparent co-curation, co-branding and co-profit sharing could become a powerful moat.

For true partnerships with farmer enterprises in the long run, you can’t only do input or output. You have to participate in the entire value chain if you want to control it.

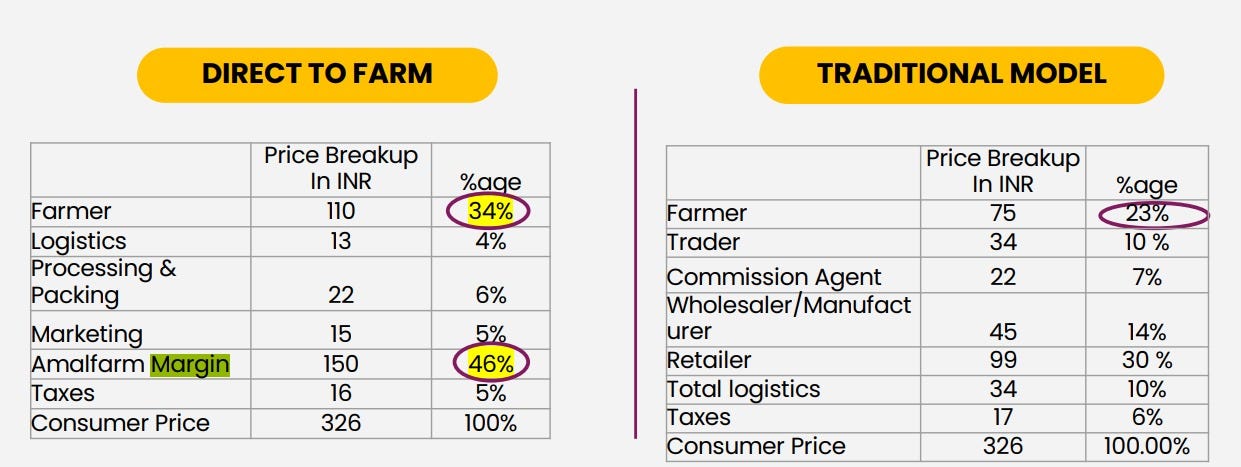

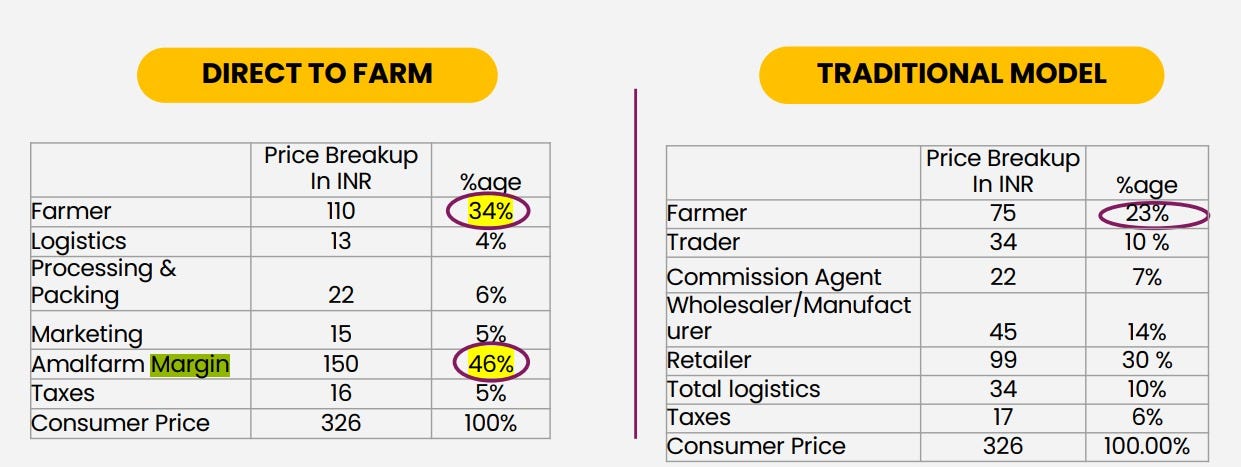

With GI Crops delivered through direct-to-farmer model, there is enough evidence that farmers are able to get 30-40% more than the traditional model.

<Image Credits: Amalfarm>

Migration among India’s wealthy salaried class has triggered a lot of nostalgia-fueled demand for place-of-origin promise products.

If the government is serious about taking ODOP produce to the global markets, can the Indian embassy in every part of the word dedicate one resource to promote place-of-origin promise products in every part of the country? Can we do generic branding better, when it comes to Indian products?

Outside India, several countries have done a great job to such an extent that third-rate products have often been marketed the first class way. In India, on the other hand, first class products have been marketed the third class way.

India has never been strong on marketing, branding, promotion. That has been our weakest link.

Several promising initiatives started by the government, including One District One Produce, need to introspect deeply on their return on investment. Rushing to put the label to gain few brownie points without doing the necessary work on the ground will not yield results.

We need more players like Telangana State Food Processing Society which has undertaken efforts to midwife FPOs with federated demand-led structures and hand hold their sourcing partnerships by building plug-and-play supply chains.

Common Facility Centers can’t be eighty kilometers away from farmer clusters, if they are serious about small farmers utilizing those infrastructures.

Government is spending a lot on promotion. Are farmers getting the market access to the market? How can we increase the success of these promotion efforts? How do we bring in next level of transparency to foster a culture of trust? Can you share the customer purchase order with an FPO?

Can we bring more clarity on the FSSAI licenses FPOs ought to have? How can we make FPOs more accountable with KRAs when a lot of FPOs exist in paper than in reality in India?

GI tagged products have deeper significance in conservation of native varieties and carry the idea and genetic material forward. It is culturally extremely important for Indians. At the same time, it is important to place checks in balance with validation and proof mechanisms to ensure that bad actors don’t hijack the GI movement.

Structurally, ONDC is a good concept. But, the user experience cracks at at both hub and node levels. Proper packaging, good images and there is a lot of hygiene improvement needed to make it work. Otherwise, it would limit to being a tool for food entrepreneurs to discover samples from farmers and farmer enterprises.

I hope you enjoy the conversation as much as I did:)

So, what do you think?

How happy are you with today’s edition? I would love to get your candid feedback. Your feedback will be anonymous. Two questions. 1 Minute. Thanks.🙏

💗 If you like “Agribusiness Matters”, please click on Like at the bottom and share it with your friend.